Orbit Without Order: The Costs of Fragmented Space Governance

By Davide E. Iannace and Maia Sacchetto, in collaboration with the Geopolitical Insight and Education Foundation

Space is no longer the exclusive domain of states and scientists. The infrastructure that now underpins navigation, communications, and military operations across the world's democracies is increasingly owned by private actors, governed by competing blocs, and subject to rules written for a world that no longer exists.

The transformation of outer space from a domain of scientific exploration into a critical arena of economic competition and geopolitical strategy marks the emergence of the “New Space” era (Dolman 2001). Once governed by a limited number of state actors within a relatively stable legal framework, space has evolved into a congested and contested environment where commercial, military, and political interests increasingly overlap.

This shift has been driven primarily by the rapid expansion of private actors, most notably SpaceX, whose technological advancements have significantly reduced the cost of access to orbit. As a result, the space economy has experienced unprecedented growth, reaching an estimated value of $626.4 billion in 2025 and projected to exceed $1 trillion within the next decade (Novaspace, 2026). Beyond its economic significance, space-based infrastructure has become a strategic asset underpinning critical terrestrial functions, including communications, navigation, and security operations - functions that democratic governments and their citizens now depend on daily, and over which those governments exercise diminishing control.

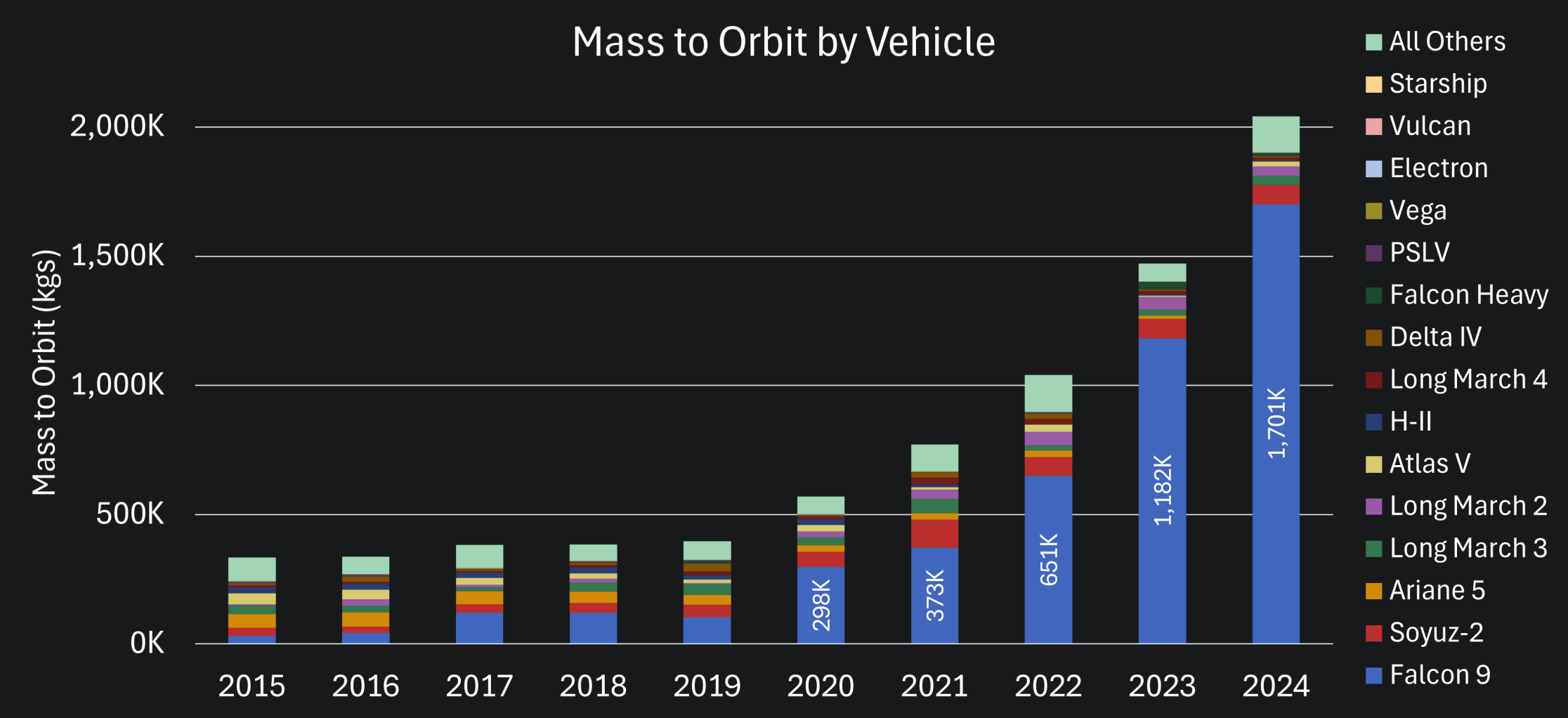

Figure 1: Mass to orbit by vehicle, trend, 2024. Source: Todd Harrison/AEI, based on BryceTech data, January 2025.

Despite this transformation, the legal and governance framework regulating space activities remains largely anchored in principles established during the Cold War, particularly the Outer Space Treaty. Those principles were foundational in promoting the peaceful use of outer space, but they were designed for a world of state actors and bilateral rivalry; and while perhaps foundational in promoting the peaceful use of outer space, these principles are increasingly ill-equipped to address contemporary challenges such as the commercialization of orbit, the proliferation of private actors, and the emerging prospect of Space Resource Utilization (SRU).

In practice, this regulatory gap is being filled now through fragmented and often competing governance initiatives - first and foremost with the Artemis Accords, reflecting a shift toward “minilateral” arrangements that risk institutionalizing asymmetries in access to space resources and capabilities;and that increasingly place the infrastructure of democratic societies outside the reach of democratic oversight.

The decisions being made now about who controls orbital infrastructure - under what rules, and accountable to whom - will shape the strategic and democratic landscape of the coming decades. That those decisions are being made largely outside democratic oversight, through bilateral memoranda and procurement contracts rather than multilateral law, is not an accident. It is the product of fifty years of governance drift, accelerated by a decade of commercial disruption that existing institutions were not built to absorb. What follows traces how that happened, where the critical failures now sit, and finally what a serious policy response would look like.

The Evolution of Space Governance

Space was never truly “governed” per se; better to say it was managed, during a narrow window when the number of actors was small enough and the stakes were defined enough that binding rules were achievable. That window closed in 1979. What has followed is not a governance system (which would suggest a comprehensive vision and policy) so much as a set of workarounds: Soft law instruments with frequently no enforcement teeth, domestic legislation projected outward by economic leverage, and bilateral alignments that serve the interests of those inside them while foreclosing options for everyone else.

The underlying tension has not changed. Space remains, in legal theory, a global commons. Yet, in practice, it is being carved up by the states and corporations with the capital and technology to act first. The multilateral frameworks that were supposed to prevent that are deadlocked. The club-based arrangements replacing them were designed to be.

The "Big Five" and the Golden Age of Space Lawmaking

The foundational corpus of international space law - the "Big Five" treaties - was produced in the context of intense US-Soviet rivalry (Gabrynowicz, 2004). The impetus was not idealism. Instead, the urgent need to prevent the militarization of outer space from escalating into an orbital nuclear theater, which would have destabilized the fragile doctrine of Mutually Assured Destruction (MAD) (Vlasic, 1991), sat at the forefront of theorists and policymakers’ minds. Operating under UNCOPUOS, established as a permanent body in 1959, international diplomacy produced a series of binding multilateral agreements intended to insulate outer space from terrestrial geopolitical conflict (Marchisio, 2019).

The indisputable constitutional cornerstone of this universalist legal order is the 1967 Treaty on Principles Governing the Activities of States in the Exploration and Use of Outer Space, including the Moon and Other Celestial Bodies, universally known as the Outer Space Treaty (OST) (United Nations, 1967). Ratified by all major spacefaring nations, the OST established the core legal framework of the domain. Article I designates space as the province of all mankind - exploration and use to be carried out "for the benefit and in the interests of all countries, irrespective of their degree of economic or scientific development" – provincia humani generis (“[...] and shall be the province of all mankind…”). Article II prohibits national appropriation: outer space, including the Moon and other celestial bodies, is not subject to national appropriation by claim of sovereignty, by means of use or occupation, or by any other means (Hertzfeld et al., 2005). It remains the primary legal barrier against territorial expansion in orbit. Article IV achieved partial demilitarisation, prohibiting states from placing weapons of mass destruction in orbit or on celestial bodies (Marchisio, 2019).

UNCOPUOS went on to negotiate three further agreements (Lyall & Larsen, 2025). The 1968 Rescue Agreement established the humanitarian obligation to assist and return astronauts in distress. The 1972 Liability Convention created a dual liability framework - absolute liability for damage caused on Earth's surface, fault-based liability for damage elsewhere (United Nations, 1972). The 1975 Registration Convention required states to provide orbital parameters for every object launched, creating a baseline of transparency and space situational awareness (Lyall & Larsen, 2025).

This architecture was fairly coherent – but it was also built entirely around states and the Westphalian assumption that sovereign governments would remain the exclusive gatekeepers of space technology and capital (Pelton & Jakhu, 2017). Article VI of the OST attempted to address this, declaring that states bear international responsibility for national activities in outer space "whether such activities are carried on by governmental agencies or by non-governmental entities," and requiring "authorisation and continuing supervision." But the treaty provides no harmonised regulatory mechanisms, no licensing standards, and no enforcement tools applicable to commercial entities (von der Dunk, 2018). In a world where private companies launch thousands of mass-produced satellites annually and routinely outpace civil space agencies in technological capability, that gap has become the central problem of space governance (Blount, 2025).

The terminal failure of the universalist model came with the fifth and final UN space treaty: the 1979 Moon Agreement (United Nations, 1979). Its drafters attempted to pre-emptively regulate commercial extraction of celestial resources through Article 11, which declared the Moon and its natural resources the "Common Heritage of Mankind." Article 11(5) mandated the establishment of an international regime to govern exploitation once it became feasible (Tronchetti, 2013).

The major industrialised nations read this as a threat to commercial investment and refused to sign. The United States, the Soviet Union, and China all declined to ratify. The Moon Agreement has only a handful of non-spacefaring signatories (Tronchetti, 2013).

That refusal marked the end of hard multilateral lawmaking in space. Since 1979, UNCOPUOS has grown from a small committee of specialised states into an ideologically polarised assembly of over 100 nations, bound by a consensus requirement that has produced effective legislative deadlock (West, 2025). The response has been a pivot to soft law - non-binding instruments, codes of conduct, and Transparency and Confidence-Building Measures (Steer, 2022).

The 2007 Space Debris Mitigation Guidelines and the 2019 Guidelines for the Long-term Sustainability of Outer Space Activities are the main products of this approach (United Nations COPUOS, 2019). While these soft law mechanisms are highly valuable for establishing baseline technical engineering standards and voluntarily harmonizing orbital safety practices, they possess no formal mandatory enforcement mechanisms, no economic penalties for non-compliance, and no binding dispute-resolution compliance architectures (Steer, 2022).Or, put simply, they have value as technical standards, but they have no enforcement mechanisms, no penalties for non-compliance, and no binding dispute resolution. In a commercial space economy where actors face immediate competitive pressures, voluntary guidelines are simply not a governance framework (Pelton & Jakhu, 2017).

“Minilateralism” and the Artemis Accords (2020-2026)

The UN stalemate did not produce a vacuum so much as an opening. When binding multilateral rules became impossible to negotiate, the United States moved to fill the space - not through the UN system, but around it.

When states cannot agree multilaterally, the temptation is to work with a smaller, more aligned group instead. That is minilateralism: prioritising speed and ideological coherence over inclusivity (Axelrod & Keohane, 1985). In cislunar space, it has become the dominant mode of governance - a mechanism for constructing parallel regulatory regimes, establishing property rights frameworks, and securing strategic supply chains outside the UN framework (Hertzfeld et al., 2005; West, 2025).

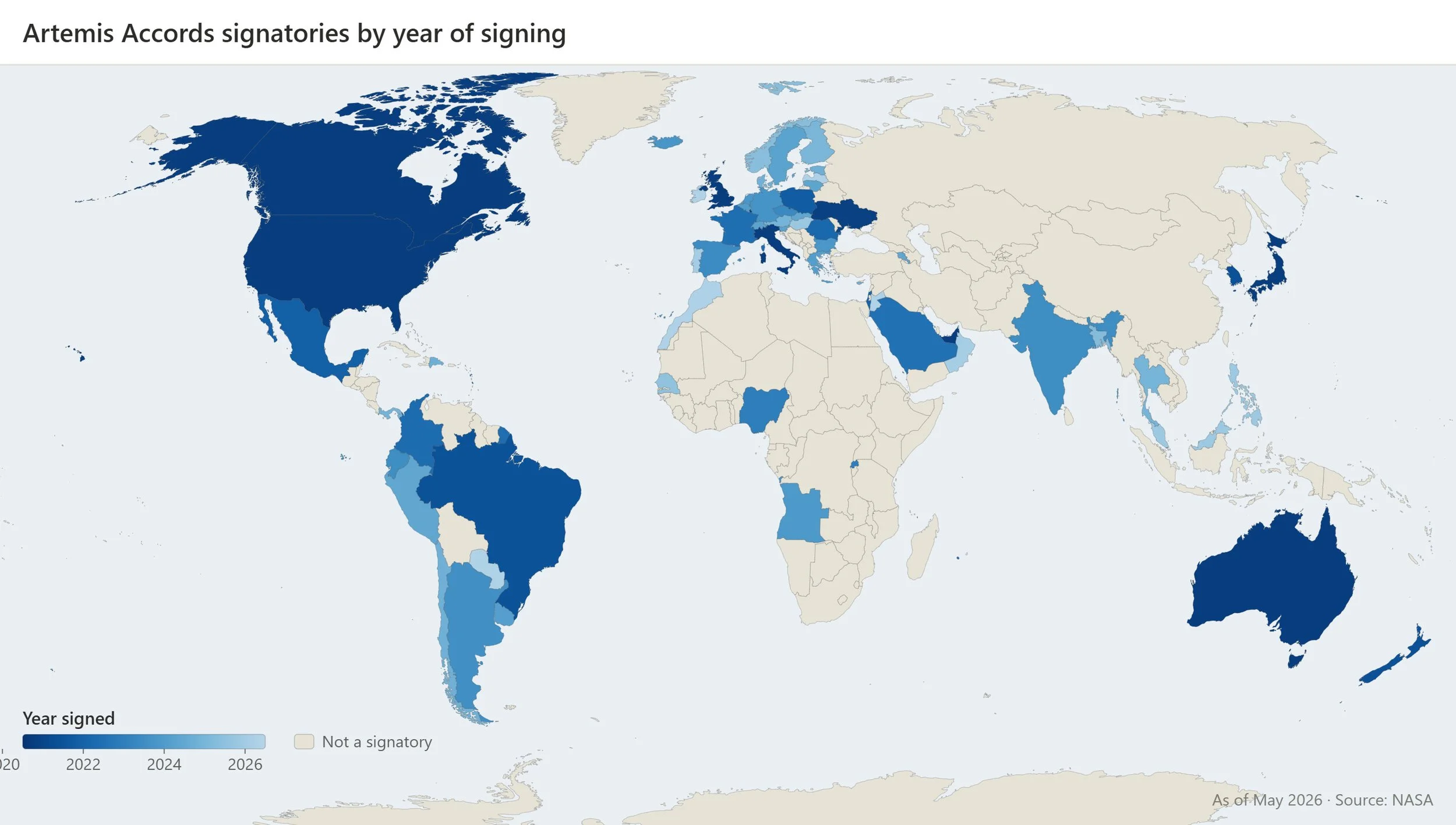

The preeminent, structurally transformative manifestation of this minilateral architecture is the Artemis Accords, an ambitious diplomatic initiative spearheaded in 2020 by the United States through the National Aeronautics and Space Administration (NASA) in close coordination with the Department of State (NASA, 2026). Formally titled The Artemis Accords: Principles for Cooperation in the Civil Exploration and Use of the Moon, Mars, Comets, and Asteroids for Peaceful Purposes, this framework has experienced massive geopolitical and diplomatic expansion, growing from its eight original founding signatories in 2020 to an expansive coalition of 67 nations as of May 2026 (NASA, 2026).

Figure 2: Artemis Accords signatory countries by year, as of May 2026. Source: NASA.

The Artemis Accords do not possess the formal legal status of a multilateral treaty; rather, they are structured as a series of identical, non-binding political commitments executed via bilateral Memoranda of Understanding (MoUs) between NASA and the respective national space agencies of the signatory states (Freeland, 2021). This legal format was deliberately selected by the United States to bypass the protracted, uncertain process of domestic senatorial ratification and to avoid the structural vetoes inherent in the UNCOPUOS consensus mechanism (West, 2025).

The Accords claim fidelity to the 1967 Outer Space Treaty. The claim is selective. Section 10 is where the reinterpretation matters most. Section 10(2) asserts that extracting space resources does not constitute national appropriation under Article II of the OST - that "the utilization of space resources, which can benefit humankind by providing necessary support for safe and sustainable operations, should be conducted in a manner that complies with the Outer Space Treaty" (United Nations, 1967; NASA, 2020). Decoupling extraction from appropriation is a political choice, backed by American weight, to guarantee private actors that celestial resources can be owned, traded, and sold (Jakhu & Freeland, 2024). It mirrors the logic of the U.S. Commercial Space Launch Competitiveness Act of 2015, which already grants American citizens the right to possess, own, transport, use, and sell resources obtained in space (US Congress, 2015). The Accords scale that domestic position into a coalition standard (Blount, 2025).

By decoupling the extraction of resources from the prohibition of territorial sovereignty, the Accords provide an explicit, pro-market, and US-backed international legal guarantee to private aerospace corporations, mining firms, and venture capital investors (Hertzfeld et al., 2005). This international minilateral strategy works in perfect lockstep with domestic American legislative frameworks, specifically the U.S. Commercial Space Launch Competitiveness Act of 2015 (Public Law 114-90), which grants US citizens the explicit right to possess, own, transport, use, and sell celestial resources obtained in accordance with applicable law (US Congress, 2015). The Artemis Accords effectively export this domestic free-market legal architecture to a global coalition of partners, creating a powerful de facto international standard (Blount, 2025).

Section 11 introduces Safety Zones - geographically bounded areas around habitats, landing pads, and extraction facilities, intended to prevent harmful interference between operators (NASA, 2020). NASA presents these as consistent with Article IX of the OST. For example, a safety zone established over the water-ice deposits at Shackleton Crater's rim - one of the most resource-rich and geographically constrained sites on the Moon - could exclude competitors under the operational language of deconfliction, with no independent body to assess whether the exclusion is justified (Blount, 2019; Murthi & Sriravamurthy, 2024). The term that recurs again and again in the literature is "creeping sovereignty."

This “minilateral” model of this club-based governance does not rely on traditional international law for its enforcement. Or put another way, compliance is not legally compelled; the idea is that it is economically incentivised. Access to NASA procurement contracts, the American aerospace supply chain, the Gateway architecture, and the Deep Space Network are, in this sense, the “rewards” for signing (West, 2025). States that sign gain access; whereas states that do not are marginalised (Pelton & Jakhu, 2017). For smaller spacefaring nations, this is less a choice than a structured and serious pressure.

Unsurprisingly, this minilateral strategy has accelerated the structural fragmentation of the global space economy, triggering defensive, parallel coalition-building by rival great powers that reject the legitimacy of American-led unilateral standard-setting (Murthi & Sriravamurthy, 2024). This fragmentation has materialized through the formal institutionalization of the International Lunar Research Station (ILRS), a competing, parallel deep-space exploration and governance architecture co-led by the China National Space Administration (CNSA) and the Russian Federal Space Agency (Roscosmos)(CNSA & Roscosmos, 2021).

Or, put more simply, China and Russia have responded in kind to the U.S.’s exclusionary tactics. The International Lunar Research Station, unveiled in 2021, is the institutional answer to Artemis (CNSA & Roscosmos, 2021). It has recruited across the Global South and Eurasian partners, promoting state-to-state egalitarianism and non-commercial control over celestial access as the alternative to what ILRS members frame as Western technological hegemony (Murthi & Sriravamurthy, 2024).

Thus, by 2026 at time of writing, there are now essentially two competing governance ecosystems with incompatible standards, incompatible legal interpretations, and incompatible visions of who space belongs to (Blount, 2025; West, 2025; Murthi & Sriravamurthy, 2024; UNOOSA, 2026). Technical interoperability, spectrum allocation, data-sharing, and property rights are no longer subjects of multilateral negotiation. They are instruments of bloc competition. The communications networks, navigation systems, and security architectures that European citizens rely on are being governed by arrangements struck without them, accountable to no shared legal order, and increasingly difficult to contest or exit.

Stratification of Space Governance

It is useful to conceive of outer space as being divided into three functionally distinct regions. Low Earth Orbit (LEO) spans roughly 160 to 2,000 kilometres above the surface - close enough for low latency, high-resolution Earth observation, and mass-market telecommunications, but requiring large constellations rather than single platforms to maintain continuous coverage, because any individual satellite circles the globe every 90 minutes (Adilov et al., 2020). Medium Earth Orbit (MEO), from 2,000 to approximately 35,786 kilometres, is historically the domain of positioning, navigation, and timing infrastructure - GPS, Galileo, GLONASS, BeiDou - and is becoming increasingly attractive for high-throughput connectivity targeting maritime, aviation, and remote energy sectors (Sander et al., 2019). Geostationary Earth Orbit (GEO), fixed at exactly 35,786 kilometres above the equator, is where a satellite's orbital period matches Earth's rotation. From the ground, it appears stationary. A single GEO satellite can cover nearly a third of the planet's surface continuously, making it the preferred orbit for broadcast television, military telecommunications, and meteorology - and, because it is a narrow ring above a fixed line, a scarce and intensely contested one (Ryan, 2022).

Outer space is thus not a single governance problem. And this has resulted in a pronounced governance imbalance, where traditional international space law is applied or more often bypassed in fundamentally different ways depending on the altitude of the operational payload (Muñoz-Patchen, 2021).

The pressures themselves are worth exploring briefly; as they are significantly conceptually different.

The problem in LEO is essentially congestion. Reusable launch vehicles and miniaturised hardware have made mass deployment supremely cheap compared to times pase, shifting the industry from single billion-dollar satellites with twenty-year lifespans toward thousands of lower-cost platforms in tightly orchestrated orbital shells (Morozova & Suvorov, 2021). The result is a commons under pressure. Because no binding international mechanism restricts how many objects a state or its licensed operators can place in orbit, every actor has an incentive to move first and occupy more. That in turn produces the potential for what’s known as the Kessler Syndrome: A cascade in which debris density triggers chain-reaction collisions, progressively rendering specific orbital shells unusable (Kessler et al., 2010); a fairly terrifying future of Low Earth Orbit clogged by debris in an increasingly dense shield that figuratively threatens to suffocate us. At the same time, in LEO, what’s known as “mega-constellations” of satellites also generate light pollution that disrupts optical and radio astronomy, and radiofrequency congestion that threatens signal integrity among neighbouring spacecraft (Lawrence et al., 2022; Grzelka, 2023).

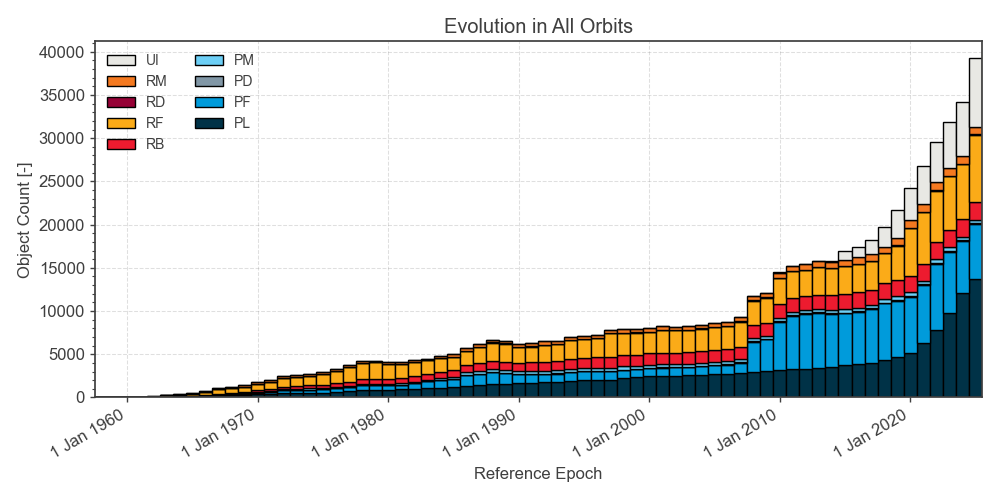

Figure 3: Growth of tracked objects in Earth orbit, 1960-2024, by category. Source: ESA Space Environment Report 2025.

The regulatory response has been fairly unilateral, which is because UNCOPUOS has not produced a binding space traffic management treaty, and thus individual states have acted alone. The most significant recent example is the FCC's "5-Year Rule," requiring satellite operators seeking US market access to de-orbit their hardware within five years of mission completion - sharply shorter than the UN's voluntary 25-year guideline (Wouters & Hansen, 2023; Jankowitsch-Preshany, 2021). It works (to the extent it does) because access to the American market is too valuable to forfeit. It is an extraterritorial projection of domestic standards through market leverage - the same mechanism the Artemis Accords use at the cislunar level.

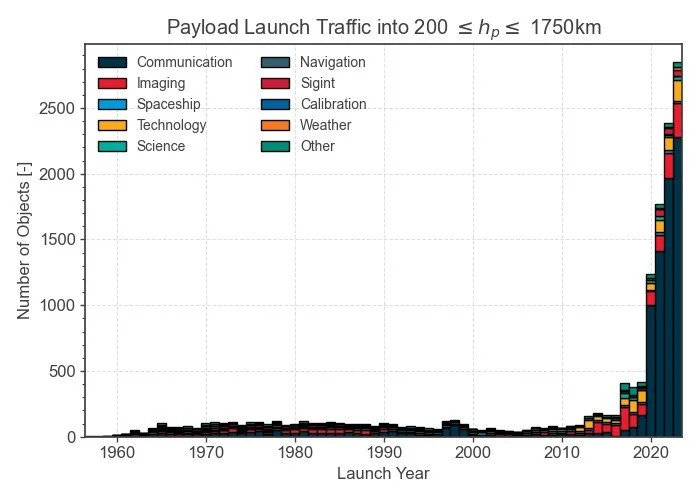

Figure 4: Payload launch traffic by category. Source: ESA Space Environment Report 2024.

In GEO, by contrast, the problem is entirely different: Scarcity, not congestion. The geostationary ring is a single narrow band above the equator, physically incapable of holding unlimited satellites without catastrophic radiofrequency interference. GEO is therefore treated as a finite resource, governed by the ITU through its Radio Regulations - a top-down allocation process in which states must secure specific orbital slots and corresponding spectrum assignments through formal coordination (Civantos-Franca, 2021; Lyall, 2022). That process has produced its own pathology: "paper satellite" registrations, where states file speculative claims for slots they lack the technology to use, purely to lock out rivals (Salin, 2024).

The result is two orbital regimes that bear little resemblance to each other. GEO retains a functioning multilateral legal order - structured, state-centric, ITU-administered, with property rights that are clearly defined and internationally recognised (Kerrest & Smith, 2023). LEO has none of that. With no binding global space traffic management treaty emerging from UNCOPUOS, leading spacefaring nations - the United States, Japan, EU member states - have written their own national space laws and used market access as leverage to project those standards outward (Blount, 2025). Private industry associations are writing collision-avoidance and data-sharing standards themselves, bypassing states entirely. The governance of LEO is defined less by diplomacy than by corporate practice and unilateral domestic enforcement, producing a multi-speed legal environment where the safety of the orbital commons depends heavily on the regulatory choices of a small number of advanced spacefaring powers (Soucek, 2022; Aoki, 2024). The navigation systems, communications infrastructure, and Earth observation capabilities that European governments and citizens depend on sit predominantly in LEO - the orbit with the least governance, and the one whose rules are being written largely without them.

Economic and Strategic Drivers of Fragmentation

Despite a fairly obvious requirement for new legislation, legislative change in space governance has been incremental. Needless to say - the change in technology has not. Private companies have operated in orbit since the 1960s - the early Comsat/Intelsat era of commercial communications satellites - but the barrier to entry has always been the same: The cost of getting hardware into orbit. That cost is, as already explained, no longer prohibitive to the government level.

Within the Western bloc, NASA has historically been the principal actor managing activities in LEO, supported by prime contractors like Lockheed Martin and Boeing, whose primary role has been to supply the equipment required for those missions. The EU and its member states have relied on a mix of European and non-European launch systems for heavy lift to orbit - the Ariane family, Soyuz, and on occasion the Space Shuttle.

There is a useful distinction to draw between two dimensions of the space economy: the commercial use of existing orbital infrastructure, and the construction of new infrastructure for commercial and non-commercial purposes.

Private actors have historically dominated the former - drawing on existing satellite constellations, or the data they generate, to support terrestrial operations. Google's use of satellite-derived data to build the mapping capabilities underpinning Google Maps is a familiar example. Direct private involvement in shaping the constellations themselves is more recent. The most prominent case is Starlink. Combined with SpaceX's reusable launch systems, which have reduced cost-to-orbit by roughly 95 per cent relative to the Space Shuttle era - from approximately USD 54,500 per kilogram to under USD 3,000 per kilogram - Starlink has established itself as the leading model of a privately held satellite constellation with a wide application range, from household broadband to support for military operations in active theatres, as observed in Ukraine.

The market consequences of that cost reduction are significant. The global space economy is currently valued at over USD 400 billion, underpinned by the breadth of satellite-delivered services - principally communications, Earth observation, and positioning. Within that sector, SpaceX has achieved a position approaching market dominance over LEO access, satellite deployment, and the provision of dual-use services. The full implications of dual-use space technology and military procurement of space services lie beyond the scope of this paper, but the operational reality is already visible: a private actor can provide - or withhold - essential systems to a military force at any stage of a conflict. The cutoff of Starlink access has been cited as one of the factors constraining Russian operations on the Ukrainian front during 2025-2026.

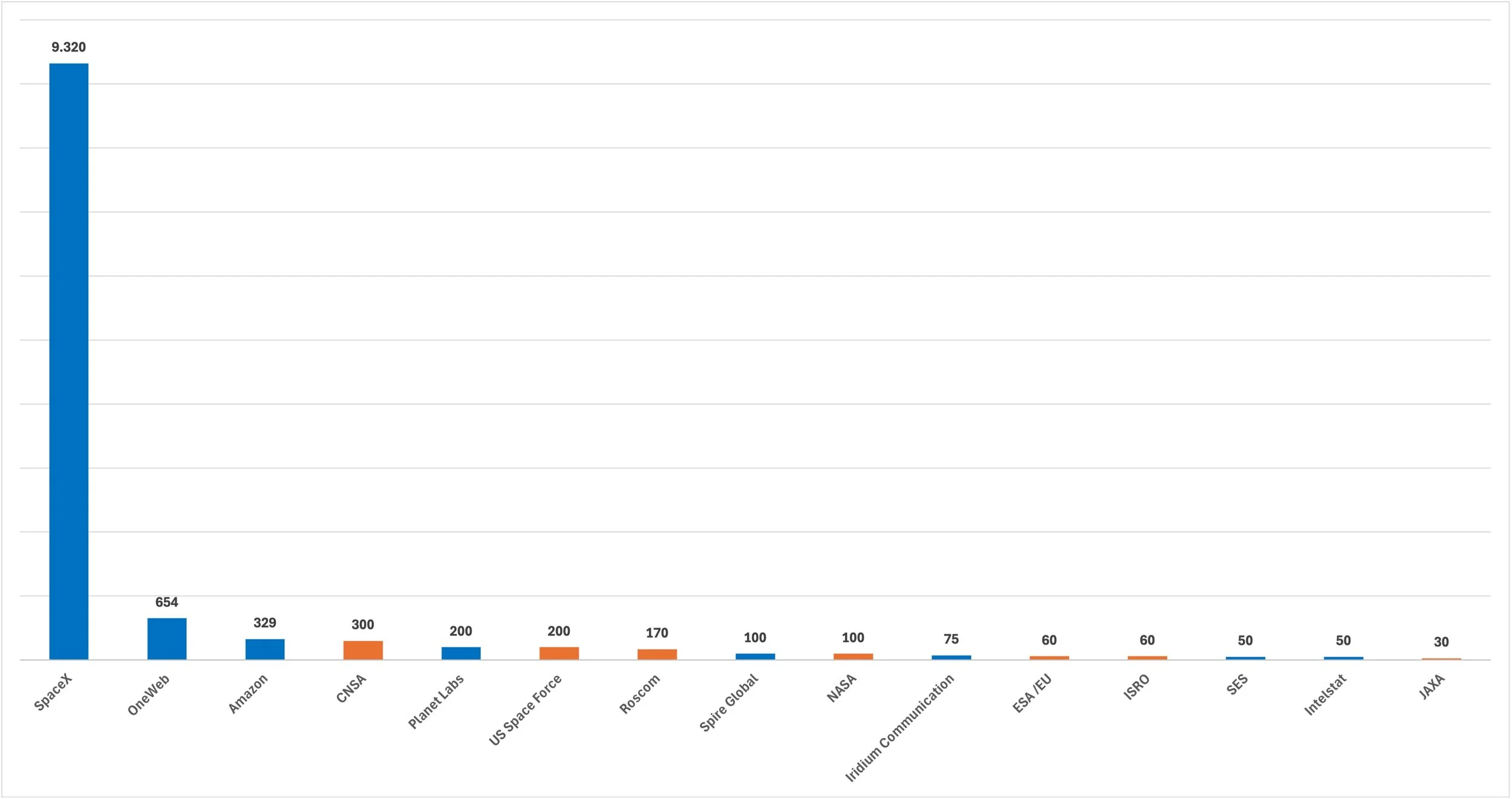

SpaceX's advantage is near-monopolistic in its breadth, covering almost the entire chain from launch vehicle to constellation operation. It is not the only actor in orbit, but it is the dominant one: Starlink alone now accounts for more than half of all active satellites in orbit, with other private operators collectively eclipsing the public-sector presence in LEO. A 2023 analysis by Dewesoft, drawing on the UCS Satellite Database, ESRI, and Space Foundation data, mapped the ownership and location of satellites in orbit at that time. Of the 4,550 satellites then tracked, only 148 among the top 32 operators were European. Germany and Finland appeared as the only independent national European operators, each with 12 satellites. The first public institutional holder in the rankings was the Chinese Ministry of Defence, with over 100 satellites, followed by the Russian Ministry of Defence with 125. The United States Air Force accounted for 87 - considerably fewer than several private operators. Satellite counts alone provide limited insight into the scope, capability, and role of individual platforms; Starlink, for instance, operates a constellation of lightweight LEO satellites designed specifically for telecommunications, whose value derives from scale rather than individual capability. The ability to deploy at that scale is directly tied to the cost reductions SpaceX's reusable launch vehicles made possible. In the three years since that analysis, the picture has shifted further in the same direction.

Figure 5: Satellites by operator, 2026. Source: OrbitalRadar.com

Reduced barriers to entry, combined with renewed strategic interest in establishing an orbital foothold for commercial purposes, are driving rapid expansion of the space economy. Private actors have been present in orbit since the 1960s, but the recent surge represents a qualitatively different trajectory: a deepening fragmentation between public and private satellite constellations. That fragmentation does not contradict the monopolistic tendency visible within what remains a highly capital-intensive market. SpaceX has lowered the barrier to entry; it has not eliminated it. The cost of placing a satellite in orbit remains substantial, and only well-resourced corporations are positioned to access orbit and market services to terrestrial actors, whether public or private.

Starlink illustrates this duality clearly. The constellation now comprises more than 10,000 active satellites in LEO. Its capacity to connect remote territories beyond cost-effective fibre-optic reach has proved attractive wherever geography drives up infrastructure costs. The central Apennine region of Italy is a practical example: limited feasibility and investment in fibre rollout across small mountain settlements has produced persistent connectivity gaps that Starlink bypasses directly, re-integrating those areas into the digital economy and enabling remote workers whose livelihoods depend on stable broadband connections.

The battlefield application is less comfortable to contemplate but impossible to ignore. According to Bloomberg, CNN, and Ukrainian outlets, Russian forces had been using Starlink terminals for both command-and-control and for guidance of long-range Shahed-derived Geran loitering munitions - providing resistance to Ukrainian electronic warfare and extending effective range. In February 2026, following Ukraine's introduction of a Starlink terminal whitelist co-developed with SpaceX, that access was disrupted. The shutdown produced significant short-term disruption to Russian operations, though independent analysts noted it was unlikely on its own to alter the war's trajectory. The episode nonetheless demonstrated something that governance frameworks have not yet adequately absorbed: a single privately controlled asset can reshape the operational logic of an entire conflict.

The Iranian case in early 2025 makes a different point about ownership. During the 12-day Iran-Israel/United States war, Iran reportedly used the TEE-01B satellite - a Chinese-built platform operated by Earth Eye Co, with ground services from Emposat - to monitor and target US military installations and infrastructure across the Gulf, according to a Financial Times investigation drawing on leaked Iranian military documents. China has denied the report. If accurate, it demonstrates how satellite assets can be decisive even when used purely for intelligence, surveillance, and reconnaissance. The critical difference between the two cases lies in who controls the asset. In Ukraine, a private company shifted the operational balance by withholding access to a commercially purchasable service. In the Iranian case, the asset was held and controlled by a state-linked Chinese commercial entity. Starlink is nominally private, but its position within US national security supply chains places it squarely within the public-private-military configuration that Mills (1956) and, more famously, Eisenhower (1961) described as the military-industrial complex. The contemporary form is arguably evolving into something more specific: a military-techno-industrial complex.

States have rediscovered what private actors never forgot. The successful Artemis II crewed lunar flyby, conducted between 1 and 10 April 2026, illustrates a renewed appetite for human exploration, combining NASA-led activity with private-sector contractors. Russian and Chinese lunar interests point to a wider non-Western re-engagement with cislunar space. The drivers are multiple. Competition between states has defined space activity since the original Cold War. The cultural weight of space remains bound to prestige: presence in orbit signals scientific capability, strategic dominance, and the capacity to access a domain that is increasingly inseparable from military and economic power. That access is, in turn, linked to the dual-use character of space infrastructure. Starlink, GPS, and comparable systems were developed for or applied to defence purposes; that interdependence is why space governance has become a priority for any actor - political or commercial - seeking influence over the flows and infrastructures of the coming decades.

Private actors, meanwhile, retain strong commercial interest in reaching orbit both as customers and as infrastructure deployers. Starlink has set the template, but it is not alone. Virgin Galactic, Boeing, Blue Origin, and others are operating in adjacent segments, including suborbital tourism and improved access to lower orbits. The plurality of public actors and private companies is itself a driver of fragmentation. Combined with the plurality of national policies and legislative regimes, it multiplies the complexity of the orbital landscape, producing a multi-layered governance environment in which legislation has only partially kept pace with public-sector developments and has lagged still further behind the rapid expansion of private activity.

The ESA's "Space 4.0" framework, introduced under Director General Jan Wörner in 2016, captures the structural character of this evolution (ESA, 2016). Space 1.0 was early astronomy; Space 2.0 the Cold War race; Space 3.0 the cooperative era of the International Space Station. Space 4.0 is defined by the diversification of actors, the integration of space into everyday digital infrastructure, and the growing role of private capital. Robinson and Mazzucato (2019) offer a complementary analysis: agencies like NASA and ESA are reframing themselves from centralised operators to ecosystem orchestrators, with miniaturisation, reusable launch vehicles, and data-centric orbital services as the underlying technological drivers. SpaceX has demonstrated what that transition looks like in practice. The digital transformation on Earth drives sustained demand for satellite-derived data that can be integrated into terrestrial applications at scale - a demand SpaceX has been uniquely positioned to meet.

The economic scale of this is quite considerable. The WEF projects the space economy will reach USD 1.8 trillion by 2035, up from USD 630 billion in 2023 - more than a twofold increase (WEF, 2024). That growth divides between two components. The backbone covers the infrastructure layer: launchers, satellites, and the tools necessary to sustain the space economy itself. The reach covers the broader set of economic activities satellites enable - communications, logistics through mapping optimisation, audiovisual connectivity in remote and underserved areas, automotive, resource extraction, and space tourism. The reach segment is projected to grow at 11 per cent annually against 9 per cent for the backbone, almost double the projected 5 per cent growth rate of the global economy. The analogy most often reached for is radio in the twentieth century, the internet at the turn of the twenty-first, or AI today - each a general-purpose driver of economic growth across sectors. Space may be something more: a multi-layered backbone enabling simultaneous growth across multiple terrestrial sectors rather than a single transformative layer.

That growth is, of course, not independent of physical supply chains. Satellites require high-end manufacturing tied to what Europe calls the critical raw materials supply chain - copper, nickel, vanadium, lithium, cobalt, all essential for aerospace development. The proliferation of new launchers, with a probable tendency toward heavy launchers, would reduce reliance on existing European launch facilities in Scandinavia and place additional pressure on fuel and materials. The CRM supply chain is therefore not peripheral to European space strategy. It is central to it - and its vulnerabilities are already visible in what has happened to semiconductor and green energy supply chains when critical material sources become geopolitically contested. The disruption of the Strait of Hormuz has contributed to sharp increases in the cost of materials like helium necessary for semiconductor production; the concentration of supply chains in Chinese or Chinese-led consortia has proved a significant strategic asset for Beijing. Space infrastructure is following the same logic, and the consequences of not addressing that dependency early are predictable from recent experience.

This can also support an understanding on how SpaceX, in its most recent IPO at Wall Street, was able to launch with a price for shares of 135 dollars. Despite the evolution of the price following various trends (rising sharply at first, then reconsolidating), the value of the company in the first impact in the public market showed a great interest of investors toward the space economy. In particular, for a company whose role is the one of providing the infrastructure for all other activities which we briefly presented above.

At the same time, another aspect to consider is the proliferation of data collection activities in orbit, and the creation of constellations capable of coordinating economic activities on Earth and enabling rapid data transfer, act as enablers for a broad range of industries - including logistics (through mapping optimisation), audiovisual connectivity (through the expansion of high-speed connections in remote and underserved areas), automotive, resource extraction, and space tourism. These are all segments that, according to the WEF 2024 analysis, stand to benefit positively from the development of a broader and more stable space economy.

So, the result is, the space economy appears to be a potential economic multiplier - not unlike radio in the twentieth century, the internet at the turn of the twenty-first century, or artificial intelligence today - each of which has acted as a driver of economic growth. The distinction, however, is that space represents a potentially multi-layered backbone for a broad range of specific sectors, offering wider opportunities across multiple segments of the terrestrial economy. And as yet, it’s the Wild West - with very little regulation to guide its development, or market protection as in other sectors.

Governance Gaps

Up to this point, we have established the broad perimeter of the space age and the space economy. We have traced a historical progression of space legislation, from the early multilateral agreements to a minilateral environment in which a different set of stakeholders is assuming a more prominent role. We have identified a shift in terms of who is involved - with private companies now able to access space with considerably greater ease than in the past - as well as the growing prominence of new state actors, such as Japan, China, and India, which are placing their own infrastructure in orbit and pursuing increasingly ambitious space programmes.

We have further noted that, whilst the space economy is on a rising trend, it is moving towards a degree of fragmentation driven by the factors described above. At the same time, it is important to highlight that there is a vertical dimension to the market structure: Certain actors, such as SpaceX, exhibit near-monopolistic tendencies, having secured control over the entire supply chain - from the preparation of launch vehicles to the creation and maintenance of satellite constellations. In this respect, a small number of companies, SpaceX foremost among them, are positioning themselves across both the backbone and reach segments of the space economy, as described by the WEF.

In short, as we have seen, the picture that emerges from the preceding sections is one of a space economy expanding rapidly under governance frameworks that were not designed for it. The legal architecture is anchored in a bygone Cold War multilateralism that assumed states as the only relevant actors and blocs governing competition; this has been utterly upended. The commercial reality is dominated by a small number of private corporations, SpaceX foremost among them, that have secured control across the entire supply chain - from launch vehicle to constellation operation - and are positioning themselves across both the backbone and reach segments of the space economy simultaneously.

The consequences are already highly visible. The number of satellites in orbit is growing rapidly across all altitudes, and most of them lack comprehensive decommissioning plans. Space debris is not a future risk; it is a present and accumulating one. The absence of consistent regulatory frameworks for satellite deployment and maintenance means that the race to occupy orbit could become the very factor that stalls or even destroys further expansion of the space economy - undermining existing investments and limiting access to more distant areas of space.

The failures of coordination are also quite myriad; from private and public entities that are accessing orbit without adequate mechanisms for collision avoidance or debris removal, to the civilian status of satellites becoming increasingly contested, as the Ukraine and Iran cases discussed above illustrate. Indeed, platforms nominally classified as commercial are being used for command-and-control, weapons guidance, and intelligence, surveillance, and reconnaissance. The line between civilian and military space infrastructure is dissolving or in some cases already dissolved, and the governance frameworks designed around that distinction are dissolving apace with it.

The underlying condition is what Hardin described as the “tragedy of the commons”. Orbit is finite - the irony of applying that concept to space notwithstanding - and its unlimited, unregulated use by an expanding set of actors with competing interests will prove detrimental to everyone, including those currently benefiting from the absence of rules. The 'space wild west' dynamic, in which each stakeholder seeks to improve its own position before constraints arrive, is not only a governance failure. It is a threat to the democratic, peaceful, and shared use of Earth's orbit that the original multilateral framework was designed to protect.

European public actors are, for now, definitively on the losing end of this dynamic. Governments are increasingly unable to regulate what is occurring in orbit - lacking both the legislative frameworks and the independent infrastructure necessary to do so. The gap is not only legislative. There is a marked absence of investment in publicly owned backbone infrastructure. ESA has launched relevant initiatives, but the response time of European public authorities has been slow, and the resources committed - in terms of coordination among national space agencies, funding, and private-sector involvement - have not been sufficient to create the conditions for meaningful European integration into space operations.

The IRIS² programme - Infrastructure for Resilience, Interconnectivity and Security by Satellite - represents the EU's most significant response to this structural vulnerability (ESA 2026). Designed to reduce dependence on non-EU constellations, IRIS² aims to strengthen European communications reliability on the reach side while building backbone presence in LEO and MEO. It is providing new resources for communication, secure data provision, and connectivity for public organisations across Europe, and the underlying rationale points in the right direction. The deployment scale, however, remains a problem. IRIS² is a small-to-medium-scale response to a large-scale challenge, and the gap between ambition and capacity is significant.

More fundamentally, IRIS² does not address the launcher problem; that is to say, the EU continues to depend on private actors - in practice, currently only SpaceX - or non-EU partners for access to orbit via heavy launchers. NASA has historically filled part of that role; the Soyuz spacecraft filled another part until the breakdown of diplomatic relations with Russia. Neither option is now reliable or strategically acceptable. European industry has legitimate demand for space operations - the EU Digital Wallet, the Digital Services Act, and REsourceEU all drive structural demand for improved data security and transfer - but so long as the infrastructure serving that demand sits in non-EU hands, the dependency is a systemic vulnerability rather than a commercial arrangement.

The analogy to supply chain concentration elsewhere is direct. The extreme concentration of lithium and cobalt supply in Chinese or Chinese-led consortia has proved to be a strategic asset for Beijing, giving it leverage over the flow of materials essential to high-end, digital, and green industries. The disruption of the Strait of Hormuz has contributed to sharp increases in the cost of helium necessary for semiconductor production. Space infrastructure is following the same logic: concentrated ownership, limited European alternatives, and governance gaps that make investment difficult to justify. The absence of clear, shared rules on orbital movements and resource use - combined with inadequate protection of satellite infrastructure, insufficient investment in cybersecurity, and supply chain vulnerability - makes investment in the European space economy a leap into the unknown. That is not a position a serious industrial and democratic power should be in, ever.

Policy Recommendations

The governance failures described in this paper are not primarily technical so much as they are political - the product of decades of institutional drift, and that compounded by a commercial disruption that arrived faster than any multilateral process could absorb. The recommendations below are calibrated to what is actually achievable in the near term. The larger strategic ambitions they point toward (strategic space autonomy) are real, but naming them without tractable first steps is not policy so much as it is wishful commentary. That said, there are four first-step actions on regulation that the EU could and indeed should consider.

1. Map and publish European dependencies on non-domestic space infrastructure.

Before any governance reform is possible, the basic facts need to be on the table. There is no comprehensive public accounting of which European public-sector functions - emergency services, navigation, secure communications, military operations - depend on infrastructure controlled by non-EU actors, under what contractual terms, and with what fallback arrangements if access is disrupted or withheld.

The first step is to produce one. The European Commission, working with ESA and member state space agencies, should commission a structured audit of public-sector dependencies on non-domestic space infrastructure, with results published in a form accessible to parliamentary scrutiny. This is not technically complex; it just requires political will to ask the question formally and make the answer public. The precedent exists in the EU's critical raw materials vulnerability assessments, which mapped supply chain exposure before proposing regulatory responses. The same methodology applies here, and the same logic justifies it: you cannot govern a dependency you have not acknowledged.

This audit would also establish the evidential basis for the conformity assessment framework described below. Without it, any assessment architecture will be built on assumptions rather than facts.

2. Extend the EU's existing risk assessment architecture to cover critical space infrastructure procurement.

The EU has developed sophisticated frameworks for assessing the risks of dependency on non-domestic technology in contexts it has already recognised as strategically sensitive - semiconductors, critical raw materials, AI systems in high-risk public-sector applications. The logic of those frameworks - identify the dependency, assess the risk, require mitigation plans, make the results auditable - applies directly to space infrastructure procurement, and the legislative architecture to extend it is already partially in place.

A practical first step is an amendment to the EU Space Programme Regulation to require dependency impact assessments for public-sector contracts above a defined threshold that involve reliance on non-EU launch, constellation, or ground segment infrastructure. The assessment need not be onerous: at minimum, it should document what function the infrastructure serves, what the fallback arrangement is if access is disrupted, and what the procurement authority's plan is for reducing the dependency over a defined timeframe. Assessments should be submitted to the European Parliament's Committee on Industry, Research and Energy and published with appropriate redactions.

This does not solve the launcher problem or close the constellation gap, of course. But it does create a formal record of the exposure and a mechanism for holding procurement authorities accountable for managing it. That is the prerequisite for everything else.

3. Develop a formal European position on space resource governance and safety zones.

The Artemis Accords are establishing de facto international standards on resource extraction and operational safety zones through coalition membership rather than multilateral negotiation. Europe has signed the Accords - and in doing so has implicitly endorsed legal interpretations of the Outer Space Treaty that remain genuinely contested. A coherent position on what those interpretations should be, and what oversight mechanisms should accompany them, does not yet exist at the EU level.

The achievable first step is a Council mandate to the European External Action Service to develop that position, in coordination with ESA and the legal services of the Commission, ahead of the next major UNCOPUOS session. The position should address two specific questions: what independent oversight mechanism should govern the establishment of safety zones on celestial bodies, and what registration and transparency requirements should apply to space resource extraction claims. Neither requires abandoning the Artemis framework or constructing a rival coalition. Both require Europe to show up with a view rather than a signature.

The Council of Europe's Framework Convention on AI demonstrates that Europe can construct governance positions that operate alongside existing instruments without requiring their replacement. The same approach is available here, and the window to shape the emerging norms rather than inherit them is closing.

4. Establish parliamentary scrutiny requirements for public-sector space infrastructure decisions with long-term strategic implications.

The democratic accountability gap in space governance is not primarily a gap in regulation. It is a gap in oversight. Procurement decisions that create long-term dependency on non-domestic private actors for functions central to public administration, security, or emergency response are currently made at executive level, often without meaningful parliamentary scrutiny or public visibility. By the time the dependency is visible, it is locked in.

The achievable first step is a procedural requirement - introduced through amendment to the Financial Regulation or equivalent national instruments - that procurement contracts above a defined value threshold involving non-EU space infrastructure for critical public functions require prior parliamentary notification and a defined scrutiny period before signature. This mirrors the existing parliamentary scrutiny mechanisms for major defence procurement in several member states, and for significant AI system deployments under the AI Act's governance architecture. It does not prevent the procurement per se but it requires that someone with democratic accountability has seen it and had the opportunity to raise concerns before the dependency is created.

This is a fairly modest ask. It is also the kind of structural change that, applied consistently over a procurement cycle, begins to shift the incentives of contracting authorities toward alternatives they currently have no formal reason to prefer.

5. Reinforce the EUSPA mandate

The current framework of the European approach into space policy is, as usual, fragmented and divided. The presence of both the European Space Agency (which is not an European Union agency) and of EUSPA (European Union Space Programme Agency) well convey the idea that current split of funding and direction in space policy is a general harm for real progress in this context. 20% of the ESA budget is coming directly from the European Union. Most of the flagship programmes of ESA are launched and managed in coordination with the European Union authorities.

But for the European Union to build a space project, and programme, which is also strongly linked with the political mandate of the Union and on its specific political goal, the presence of an independent agency can prove to be more a limit than a benefit. For this, the Union should rework the mandate of the EUSPA, to increase its legitimacy as independent actors fostering the space economy of the Union. For the EUSPA to become a powerhouse, it means improving funding availability (creating specific funds to gather private and public capitals for space activities), agency control over its programs (defining a specific governance board and structure to define priorities, expenses), linking its decisional power directly to the authorities of the Union, and developing its own capabilities outside of other supranational or non-EU agencies.

Europe, as a Union, needs to reinforce its space projection. To do so, it must maintain a grip on the future of space programmes. To maintain a democratic outlook, it needs also to link such design to democratic processes, transparency, and to an oversight by political authorities. To maintain the current democratic approach, it needs to be independent from any non-EU actors, relying on its own infrastructure for all the possible phases (from design to launch and maintenance).

The achievable first step is a revision of EUSPA's founding regulation to expand its mandate explicitly to cover strategic programme oversight - not just the operational management of existing programmes like Galileo and Copernicus, but the definition of priorities and the allocation of resources across the EU's space activities. This would require a defined governance board with representation from the Commission, the Parliament, and member state space agencies, and a reporting line to the Parliament's Committee on Industry, Research and Energy equivalent to that which governs other EU agencies with strategic mandates.

This does not require dissolving ESA or resolving the broader EU-ESA relationship in a single legislative act - that is a longer-term negotiation. What it does require is that the EU stops governing its own space interests through an agency whose accountability runs to intergovernmental rather than democratic structures. A stronger EUSPA with a clear mandate, dedicated funding instruments capable of attracting private capital alongside public investment, and direct accountability to EU political authority is the institutional prerequisite for everything else in these recommendations to be implemented coherently.

Figures

Figure 1: Mass to orbit by vehicle, 2024. SpaceX's Falcon 9 delivered 84% of total satellite mass to orbit globally that year. Source: Todd Harrison, Space Trends in 2024, American Enterprise Institute, January 2025, based on BryceTech data. Available here.

Figure 2: Artemis Accords signatory countries by year, as of May 2026. The framework grew from 8 founding nations in 2020 to 67 signatories. Source: NASA, Artemis Accords: Acceding Nations and Cumulative Progress Update, May 2026. Available here.

Figure 3: Growth of tracked objects in Earth orbit, 1960-2024, by category. Debris fragments now match or exceed active payloads at heavily used altitudes. Source: ESA, Space Environment Report 2025. Available here.

Figure 4: Payload launch traffic into low-Earth orbit, by category, over time. Source: ESA, Space Environment Report 2024. Available here.

Figure 5: Active satellites in orbit by operator, 2026. SpaceX's Starlink accounts for approximately 69% of all active satellites globally. Source: OrbitalRadar.com, Satellites by Operator, 2026. Available here.

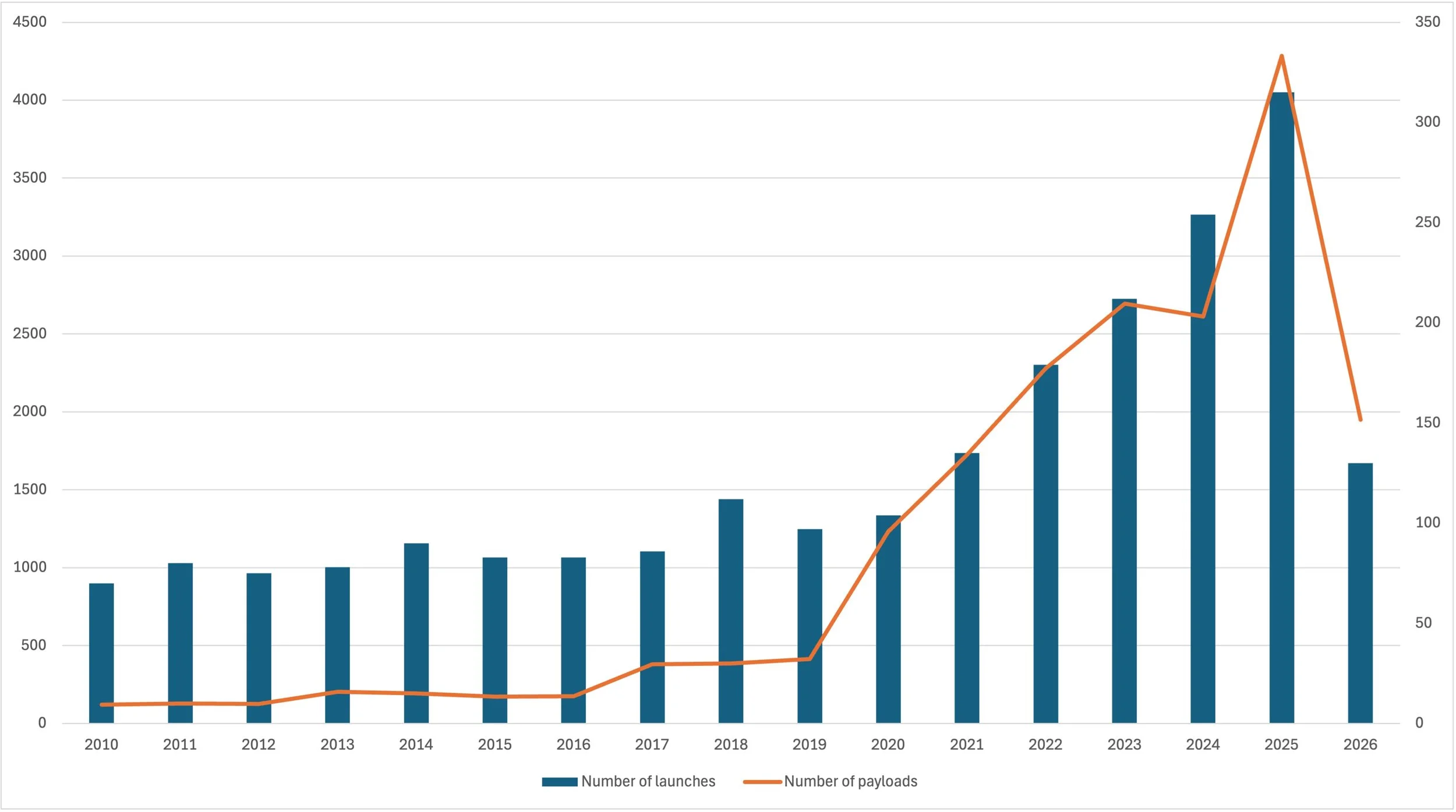

Figure 6: Number of orbital launches and payloads deployed globally, by year, as of June 2026. Source: Space-Track.org. Available here.

References

Adilov, B., Alexander, P.J. and Cunningham, B.M. (2020) 'An economic analysis of Earth orbit pollution, economic growth, and debris mitigation', Environmental and Resource Economics, 77(2), pp. 245–271. [Available here]

Aoki, S. (2024) 'National space legislation in Asia-Pacific countries: Mitigating fragmentation in the New Space era', Space Policy, 67(1), pp. 12–25. [Available here]

Axelrod, R. and Keohane, R.O. (1985) 'Achieving cooperation under anarchy: Strategies and institutions', World Politics, 38(1), pp. 226–254. [Available here]

Blount, P.J. (2019) Reprogramming the World: Cyberspace and the Geography of Global Order. Bristol: e-International Relations Press. [Available here]

Blount, P.J. (2025) Global Space Governance: From Treaties to National Laws. Oxford: Oxford University Press.

Brzozowski, A. (2025) Securing the High Ground: EU Defense Policy in the Space Domain. Brussels: CEPS Policy Brief.

China National Space Administration (CNSA) & Roscosmos (2021) International Lunar Research Station (ILRS) Guide for Partnership. Beijing/Moscow: CNSA/Roscosmos. [Available here]

Civantos-Franca, J. (2021) 'The ITU coordination procedure for geostationary satellites: Balancing sovereign rights and commercial efficiency', Air and Space Law, 46(4), pp. 415–438. [Available here]

Dewesoft (2023) Every Satellite Orbiting Earth and Who Owns Them. [Available here]

Dolman, E.C. (2001) Astropolitik: Classical Geopolitics in the Space Age. London: Routledge. [Available here]

European Parliament (2025) Report on the Future of EU-US Space Cooperation: Navigating the Artemis Accords. Committee on Foreign Affairs (AFET). Brussels: European Parliament.

European Space Agency (2026) In-Orbit Servicing and Manufacturing (ISAM): European Strategic Roadmap. ESA.

Freeland, S. (2021) 'The Artemis Accords and the future of international space law', Air and Space Law, 46(3), pp. 263–288. [Available here]

Froehlich, P. (2023) The European Union's Approach to Space Traffic Management: Regulatory Ambitions and Geopolitical Constraints. Cham: Springer. [Available here]

Gabrynowicz, J.I. (2004) 'Space law: Its Cold War origins and challenges in the era of globalization', Suffolk University Law Review, 37(4), pp. 1041–1065. [Available here]

Grzelka, M. (2023) 'Economic tools for the governance of outer space commons: Fees, quotas, and tradeable launch rights', Journal of Space Safety Engineering, 10(3), pp. 189–201. [Available here]

Hertzfeld, H.R., von der Dunk, F.G. and Salin, P.J. (2005) 'Bringing space law into the commercial world: Property rights without sovereignty', Chicago Journal of International Law, 6(1), pp. 81–99. [Available here]

Jakhu, R.S. and Freeland, S. (2024) 'The relationship between the Outer Space Treaty and the Artemis Accords', Journal of Space Law, 48(1), pp. 89–116.

Jankowitsch-Preshany, I. (2021) 'International space traffic management: Standard-setting outside the United Nations', German Journal of Air and Space Law (ZLW), 70(2), pp. 214–231.

Kerrest, A. and Smith, L.J. (2023) 'The geostationary orbit: A closed legal circle under technical strain', Journal of Space Law, 47(2), pp. 154–178.

Kessler, D.J., Johnson, N.L., Liou, J.C. and Matney, M. (2010) 'The Kessler Syndrome: Implications for future space operations', Advances in the Astronautical Sciences, 137(1), pp. 47–62. [Available here]

Lawrence, A., Rawlins, S.J., Houghton, P.J. and Watson, F. (2022) 'The impact of satellite mega-constellations on astronomical observations: Economic and regulatory dimensions', Nature Astronomy, 6(4), pp. 411–417. [Available here]

Lyall, F. (2022) 'The International Telecommunication Union: A unique international organization under pressure', Leiden Journal of International Law, 35(3), pp. 601–622. [Available here]

Lyall, F. and Larsen, P.B. (2025) Space Law: A Treatise (3rd edn). London: Routledge. [Available here]

Macauley, M.K. (2006) 'The economics of space law', Chicago Journal of International Law, 7(1), pp. 211–224. [Available here]

Marchisio, S. (2019) Law in Outer Space. Rome: Giappichelli.

Morozova, E. and Suvorov, S. (2021) 'Legal challenges of large satellite constellations in Low Earth Orbit: A Russian perspective', Space Policy, 56, article 101421. [Available here]

Muñoz-Patchen, C. (2021) 'Regulating the space commons: Treating orbit as an environmental resource', Harvard Environmental Law Review, 45(2), pp. 497–535. [Available here]

Murthi, K.R. and Sriravamurthy, P. (2024) 'Geopolitical fragmentation of space governance: Assessing Artemis vs. ILRS paradigms', Space Policy, 68(2), pp. 101–114. [Available here]

NASA & US Department of State (2020) The Artemis Accords: Principles for Cooperation in the Civil Exploration and Use of the Moon, Mars, Comets, and Asteroids for Peaceful Purposes. Washington, DC: NASA. [Available here]

NASA (2026) Artemis Accords: Acceding Nations and Cumulative Progress Update, May 2026. Washington, DC: NASA Office of International and Interagency Relations. [Available here]

Novaspace (2026) Space Economy Report 2026: A Structural Inflection Point. Novaspace.

Pelton, J.N. and Jakhu, R.S. (eds.) (2017) Global Space Governance: An International Study. Cham: Springer. [Available here]

Rao, A., Burgess, M.G. and Kaffine, D. (2020) 'Orbital-use fees could more than quadruple the value of the space industry', Proceedings of the National Academy of Sciences (PNAS), 117(24), pp. 13390–13395. [Available here]

Robinson, D.K.R. and Mazzucato, M. (2019) 'The evolution of mission-oriented policies: Exploring changing market creating policies in the US and European space sector', Research Policy, 48(4), pp. 936–948. [Available here]

Ryan, J. (2022) The Geopolitics of the Geostationary Orbit: Allocating Scarcity in Telecommunications. London: Palgrave Macmillan. [Available here]

Salin, P.J. (2024) Satellite Communications and the ITU Regulatory Architecture: Twenty Years of Commercialization. Montreal: McGill Centre for Research in Air and Space Law.

Sander, K., Meyer, L. and Schmidt, T. (2019) 'Navigation constellations and MEO governance: Security vs. open access', International Studies Perspectives, 20(3), pp. 284–306. [Available here]

Soucek, A. (2022) Space Law Essentials: Volume 2 – Legal Regimes for Specific Space Activities. Vienna: Linde Verlag.

Steer, C. (2022) Mitigating Security Risks in Space: The Role of Soft Law and Lex Gardenia. Oxford: Oxford University Press.

Tronchetti, F. (2013) The Exploitation of Natural Resources of the Moon and Other Celestial Bodies: A Proposal for a Legal Regime. Leiden: Martinus Nijhoff Publishers. [Available here]

Ukrainska Pravda (2026) [Available here]

United Nations (1967) Treaty on Principles Governing the Activities of States in the Exploration and Use of Outer Space, including the Moon and Other Celestial Bodies (Outer Space Treaty). 610 UNTS 205. [Available here]

United Nations (1972) Convention on International Liability for Damage Caused by Space Objects (Liability Convention). 961 UNTS 187. [Available here]

United Nations (1979) Agreement Governing the Activities of States on the Moon and Other Celestial Bodies (Moon Agreement). 1363 UNTS 3. [Available here]

United Nations COPUOS (2019) Guidelines for the Long-term Sustainability of Outer Space Activities. A/AC.105/2019/L.5. [Available here]

UNOOSA (2026) Updated Draft Set of Recommended Principles for Space Resource Activities. United Nations Office for Outer Space Affairs, April 2026. [Available here]

US Congress (2015) U.S. Commercial Space Launch Competitiveness Act. Public Law No. 114-90. [Available here]

Vlasic, I.A. (1991) 'The Space Treaty: A preliminary evaluation after twenty-three years', Space Policy, 7(2), pp. 112–124. [Available here]

von der Dunk, F.G. (2018) Advanced Introduction to Space Law. Cheltenham: Edward Elgar Publishing. [Available here]

Weeden, B. and Samson, V. (eds.) (2023) Global Space Governance: A New Analytical Architecture for the 21st Century. Washington, DC: Secure World Foundation. [Available here]

West, J. (2025) 'Minilateralism as the new norm: U.S. hegemony and coalition-building in cislunar space', International Studies Quarterly, 69(1), pp. 45–59. [Available here]

World Economic Forum (2024) Space: The $1.8 Trillion Opportunity for Global Economic Growth. [Available here]

Wörner, J. (2026) European Space Strategy 2030: From Vision to Regulation. Vienna: European Space Policy Institute (ESPI).

Wouters, J. and Hansen, R. (2023) 'Unilateral projection of space safety norms: The FCC's 5-Year Rule and international law', Journal of Air Law and Commerce, 88(2), pp. 241–269.